Why Most People Who Consolidate Their Debt End Up With Twice as Much

By Your Debt Advocate · Updated 2026

The pitch for debt consolidation sounds clean. One loan instead of five. One payment instead of five. One fixed end date instead of an open-ended pile.

Most families who hear that pitch take it. It feels like the responsible move.

Three years later, most of those same families are carrying both the consolidation loan AND fresh balances on the cards they "paid off." They didn't fix their debt. They doubled it.

Here is why that happens to so many honest people, and how to know if consolidation is actually the right tool for your family or the trap your bank is selling.

What Debt Consolidation Actually Is

Debt consolidation is straightforward. You take out one new loan. You use the proceeds from that loan to pay off all your existing credit cards. Now you have one debt — the consolidation loan — instead of five separate card balances.

The new loan is usually one of three kinds:

- Personal loan from a bank. Fixed term (3-7 years), fixed monthly payment, fixed interest rate.

- Personal loan from an online lender. Same structure as a bank personal loan, often with faster approval and slightly higher rates.

- Balance transfer card. A new credit card with a 0% introductory APR for 12-21 months. You move card balances onto the new card and try to pay them off before the promo period ends.

The math sounds attractive on paper. Cards charge 22-29% APR. Personal loans charge 9-18%. A balance transfer charges 0% for the promo window. Replace the high-rate cards with a lower-rate loan and you save money on interest.

That math is real. The problem is the math assumes one thing that almost never holds.

The Assumption That Wrecks the Plan

Consolidation only works if you never use the cards again.

Read that again. The entire upside depends on the cards staying at zero.

Here is what actually happens. The day after you pay them off:

- Your card balances drop to zero across all five cards

- Your available credit looks great — sometimes higher than before, since the cards stay open

- Your credit utilization ratio falls. Your credit score may go up.

- Your card companies see you as a "responsible" customer again. Some send you credit limit increases in the mail within 60 days.

- You feel relieved. The crisis is over. You "fixed" it.

None of that is your fault. It is the system working exactly the way the system is designed to work.

The Double Jeopardy Trap

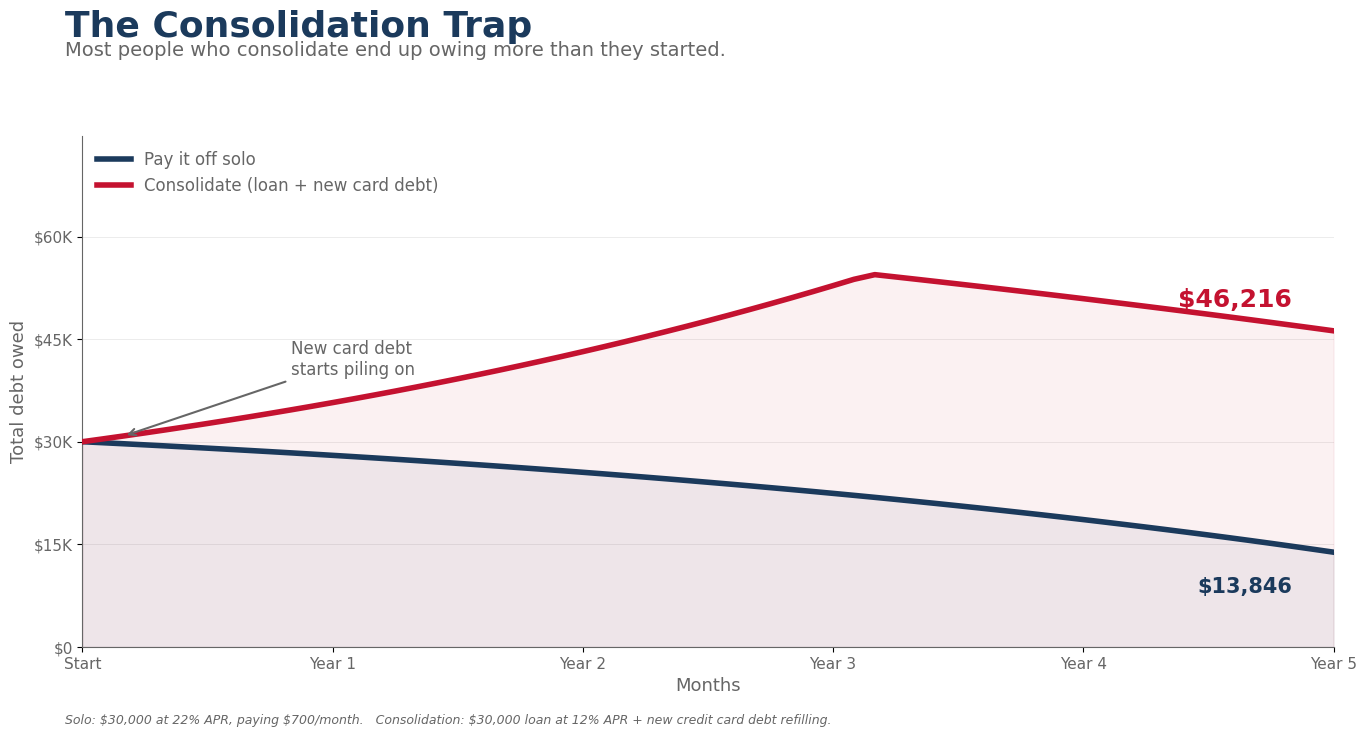

Now picture six months later. Your kid needs new tires. Your dishwasher dies. Your spouse has an emergency dental procedure. Something always comes up.

The cards are open. They have available credit on them. You tell yourself you'll pay it off next month. You put the dishwasher on the card.

Next month a different bill hits. You put that one on the card too.

Within 12-18 months, the cards are back to where they were before the consolidation. Now you have:

- The consolidation loan with 4-6 years still left on it

- Card balances climbing back to where they started

- A monthly debt service that is now higher than before consolidation

- Your credit utilization climbing again, dragging the score back down

This is the double jeopardy trap. You did the responsible thing — and ended up with more debt than you started with.

Consumer credit research has found that roughly one-third of consolidation borrowers re-accumulate credit card balances within 12-18 months of consolidating, and the share grows from there over the years that follow. The trap is common enough that lenders and counselors plan around it.

If you consolidate, close the cards the same day. Not next week. Same day. The window between paying them off and closing them is where the trap snaps shut.

Who Consolidation Actually Works For

The trap is the rule, but consolidation does work for a narrow group of families. If you fit ALL of these, it can be the right tool:

- Strong credit going in (typically 700+ FICO) — you'll qualify for a meaningfully lower rate

- Stable income that comfortably covers the loan payment

- Cards used as a tool, not as a stretch — the original card debt was a one-time event (medical bill, divorce, business gap), not a pattern

- Willingness to close all the cards the same day they hit zero

- An emergency fund of at least 3 months' expenses BEFORE the consolidation, so the next surprise expense doesn't hit a card

If you fit all five, consolidation moves you from a 22% interest rate to maybe 10%. That is real money saved over a 5-year payoff.

If you don't fit all five, consolidation usually walks you into the trap.

The Pros — Real When the Conditions Hold

- Lower interest rate. Personal loans typically save 5-15 percentage points over card APRs. On $25,000 of debt, that is significant savings over a 5-year payoff.

- One payment instead of five. Less mental load, fewer chances to miss a due date.

- Fixed end date. A 5-year personal loan has a date when it is fully paid off. Cards do not.

- Possible credit score lift. Paying cards to zero drops utilization. The lift is usually 30-60 points within 60-90 days, IF you don't refill the cards.

- Easier budgeting. One known monthly payment is easier to plan around than minimum payments that change with balances.

The Cons — Where Most Families End Up

- The trap above. Roughly one-third of consolidation borrowers re-accumulate card balances within 12-18 months, with the share growing in the years that follow.

- Origination fees. Personal loans often charge 1-8% of the loan amount up front. On $25,000, that's $250-$2,000 you finance into the loan.

- You may extend the timeline. A 5-year personal loan stretches debt that you could have paid in 4 with the avalanche method. The lower rate makes the monthly cheaper, but the total interest paid can be higher if the term is longer.

- You don't reduce the principal. You still owe every dollar. Consolidation moves the math around. It does not erase any of it.

- Your credit took a hard pull. Personal loans require a hard credit inquiry. Several inquiries from shopping multiple lenders can drag the score temporarily.

- Late on the new loan = no recovery. Miss two months on a personal loan and the lender can charge it off and refer it to collections. Cards have more flexibility in the early stages of delinquency.

The Bank's Side of the Pitch

Here is what the bank gets from selling you a consolidation loan that nobody mentions during the pitch.

The bank gets a fixed-rate, secured-against-your-paycheck-via-autodebit loan that pays them back guaranteed interest for 5 years. They get an origination fee up front. They get a customer who is now visible to them as someone who carries a lot of debt — which means they can target them for more offers later.

If you re-accumulate card debt during those 5 years (and most people do), the bank also gets the card revenue. Many of the biggest consolidation lenders are also card issuers. The trap that hurts you helps them at both ends.

None of that is illegal. None of that is hidden. It is just not in the pitch.

The Honest Comparison: Consolidation vs. The Other Paths

| Path | Reduces principal? | Best for | Re-accumulation risk |

|---|---|---|---|

| Pay cards down yourself (avalanche) | No | Under $10K, stable income | Same risk — but you keep the cards visible the whole time |

| Credit Counseling (DMP) | No | Under $10K, stable income | Low — cards are closed/frozen during the plan |

| Consolidation | No | Strong credit, perfect discipline | High — cards are paid off but stay open |

| Debt Forgiveness | Yes — typically settles for less than face | $10K+ unsecured, can't realistically pay full | None — accounts close as part of the process |

| Bankruptcy | Yes — discharges most unsecured debt | Genuinely no other option | None — debts are legally discharged |

Notice the column on re-accumulation risk. Consolidation is the only path on the list where the cards stay open and accessible after the move. Every other path either closes them, freezes them, or removes the balance entirely.

That single difference is what makes consolidation the highest-trap-risk path in the lineup.

The Math: $25,000 of Card Debt, Three Endings

Walk through what actually happens to a family with $25,000 in card debt.

Ending A: Disciplined Consolidation

Family takes a $25,000 personal loan at 12% APR over 5 years. Closes all cards the same day they hit zero. Builds a $5,000 emergency fund within 6 months. Pays the loan in full on schedule. Total paid: roughly $33,500 (standard amortization confirms: $556/month × 60 months = $33,367). Time to debt-free: 5 years.

Ending B: Trap Consolidation (the common ending)

Same loan. Cards stay open. Within 18 months, $12,000 has rebuilt across the cards. Family now owes $20,000 on the personal loan plus $12,000 on cards = $32,000 of active debt. Adds another 4-5 years of card payoff on top of the loan. Total paid over time: roughly $52,000+ depending on how the cards are managed. Time to debt-free: 9-10 years.

Ending C: Debt Forgiveness Instead

Same starting debt. Family enrolls in a debt forgiveness program. Over 32 months, accounts are settled for an average of 50-55% of face value. Total paid (including specialist fee): approximately $16,000-18,000. Time to debt-free: 32 months.

The disciplined consolidation costs about $33,500 over 5 years.

The trap consolidation costs about $52,000+ over 9-10 years.

The forgiveness path costs about $16,000-18,000 over under 3 years.

That's why the question isn't "is consolidation better than nothing?" The question is "which of these endings is most likely for your specific family?"

Three Honest Tests Before You Consolidate

Before signing any consolidation loan, run your situation against these three tests.

Test 1: Will I close the cards same-day?

Not "soon." Not "next week." Same day the cards hit zero. If the answer is anything but yes, the trap is your most likely ending.

Test 2: Do I have an emergency fund?

If your savings is under one month of expenses, the next surprise will hit a card. The cards will refill. The trap snaps shut. Build the emergency fund FIRST or pick a different path.

Test 3: Was the original card debt a one-time event or a pattern?

If your card debt came from a single shock — a medical bill, divorce, business gap, layoff — and your normal life doesn't run on cards, consolidation can work. If your card debt accumulated month after month from regular expenses outpacing income, consolidation just resets the trap.

The Bottom Line

Debt consolidation works for a narrow group of families with strong credit, stable income, an emergency fund, and the discipline to never touch the cards again.

For most families with $10,000+ in unsecured card debt, consolidation walks them into the double jeopardy trap. They end up with the new loan AND fresh card balances within 3 years. Their total debt grows, not shrinks.

If your numbers fit the narrow window, consolidation is a real tool. If they don't — and most don't — debt forgiveness or a structured do-it-yourself avalanche beats it on every measure that matters.

What To Do Next

- Run the three tests above. If you pass all three, consolidation may fit. If you fail any, pick a different path.

- Don't apply yet. Multiple loan applications create multiple hard credit pulls. Get an honest comparison first.

- If you decide to consolidate, plan the card-closure step BEFORE the loan funds. Not after.

- Take the Free Debt Relief Assessment. A senior specialist will compare consolidation against your other paths in plain English. No cost. No obligation.

Common Questions About Debt Consolidation

Will consolidation hurt my credit?

Short term, yes — the hard inquiry from the loan application drops the score 5-10 points. Within 60-90 days, paying cards to zero usually lifts the score 30-60 points. The net effect is usually positive in 90 days IF you don't refill the cards.

What credit score do I need to qualify?

Personal loans for consolidation generally require a 660 FICO minimum. The best rates start at 720+. Below 660, the rates available may not be lower than your current card rates — at which point consolidation defeats the purpose.

What about a balance transfer card with 0% APR?

Same trap mechanics, same warning. The 0% promo runs 12-21 months, then resets to 19-29% APR on whatever balance remains. If you don't pay the full transferred balance before the promo ends, you end up paying card-level interest on the balance and possibly the original cards if you've used them again.

Should I close the cards before or after the consolidation funds?

Same day the loan funds and pays them off. Not before — the consolidation loan needs the existing balances to size correctly. Not after — every day the cards stay open with $0 balances is a day they can be used. Same day.

Is the origination fee worth it?

Run the math both ways before signing. A $25,000 loan with a 5% origination fee charges $1,250 up front (often rolled into the loan). Compare the all-in cost to alternatives — credit counseling has lower up-front costs. Debt forgiveness charges nothing until settlements close.

What if I get into the trap — what's my next move?

If you have the consolidation loan AND fresh card balances, the situation has shifted. Now you have unsecured card debt AGAIN that may qualify for debt forgiveness (the personal loan is also unsecured and can be included in some cases). A senior specialist can review the new totals and tell you what fits.

Sources & References

Federal Reserve consumer credit data (G.19) and Consumer Credit Panel. Consumer Financial Protection Bureau, debt consolidation and personal loan research (~one-third re-accumulation within 12-18 months in available studies). Federal Reserve Board / Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit. FICO published credit score impact data.

This article is for consumer education only. It is not legal or financial advice. Your Debt Advocate is not a law firm, financial advisor, or lender. Every household's situation is different. A senior debt specialist can review your numbers through the Free Debt Relief Assessment.

Find Out If Consolidation Actually Fits Your Family

The math on consolidation depends entirely on your specific numbers and your specific situation. A senior specialist will run your numbers honestly — including the alternatives — and tell you which path actually fits. No cost. No obligation.

Free Assessment

Find out if consolidation fits your numbers — or if you'd be walking into the trap. A senior specialist will tell you straight.

The trap snaps shut between the day the cards hit zero and the day you close them. That window is your whole strategy.