What Your Debt Is Actually Costing You and Your Family

By Your Debt Advocate · Updated 2026

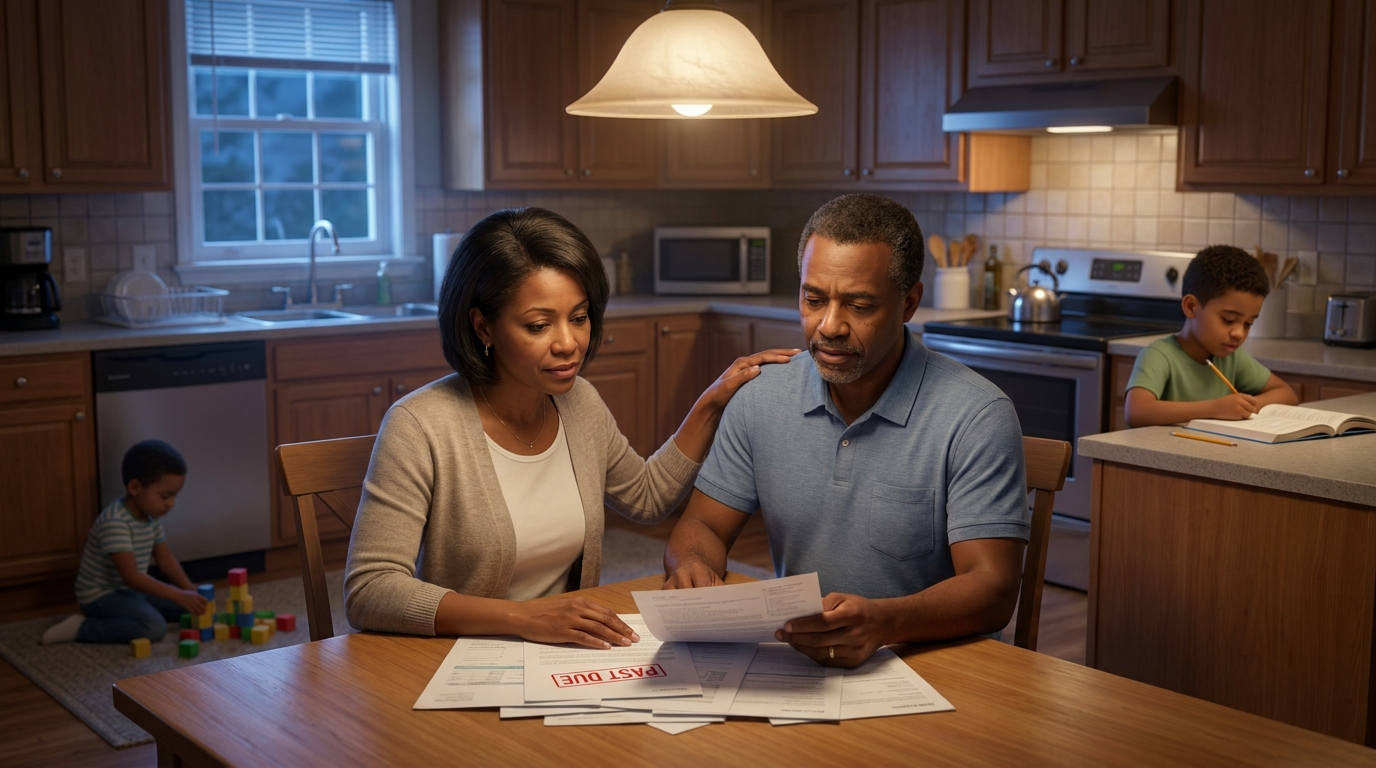

The visible cost of consumer debt is the number on the bottom of your statement. The minimum payment. The interest charge. The balance.

The real cost is everything else.

It's the conversation you didn't have with your spouse last night because you were too tired and too anxious. It's the tone your kids picked up on at the dinner table without knowing why. It's the trip you skipped, the surgery you delayed, the night class you didn't sign up for. It's what your kids will think is normal about money in 20 years.

This is the cost the credit card industry's ads don't show you. And it's usually the bigger number.

The Quiet Toll on a Marriage

Money is the most common cause of conflict in American marriages. The data on this is consistent across decades of research.

of recently divorced couples in a debt.com survey said credit card debt played a role in ending their marriage — up from 34% the year before, and 29% two years prior. (debt.com 2025 Debt and Divorce Survey.)

of Americans say a partner's debt is a reason to consider divorce. (CNBC Select / National Debt Relief survey.)

Couples who carry serious debt fight about it more. They hide purchases from each other more. They have less sex. They sleep worse. They are statistically more likely to divorce.

This is not because debt makes people bad partners. It is because chronic financial stress wears down even strong partnerships. Decisions that should be small — eating out, replacing a worn-out appliance, signing a kid up for soccer — become loaded. Every decision carries the question of whether the family can actually afford it. The default answer becomes "no." The "no" piles up. Resentment builds in directions neither person consciously chose.

None of that is a moral failing. It's the predictable result of carrying a financial burden that grew faster than either spouse expected.

The Daily Friction You Probably Stopped Noticing

If you've been carrying serious debt for a while, your nervous system has probably adapted to it. The cortisol level that used to feel like an emergency now just feels like Tuesday.

Walk through a typical week. Notice how often these moments happen:

- Picking up your phone, seeing a notification from the credit card app, and not opening it

- Choosing the gas pump that's 3 cents per gallon cheaper because every dollar matters now

- Making a purchase on a card and immediately calculating "if I pay this off when I get paid Friday, how much interest is that"

- Lying in bed at 2 AM running mental math on what bills are due when

- Avoiding a conversation with your spouse about a purchase one of you wants

- Snapping at your kids over something small and realizing it wasn't really about that small thing

- Feeling a flash of resentment toward a friend whose finances seem easier than yours

- Telling yourself "next month will be easier" when you know it won't

None of these moments is dramatic on its own. The drama is in how many of them happen in a week, and how invisible they've become to you.

This is the mental load consumer debt charges in addition to the interest. The household's worry budget gets quietly drained while the financial budget gets the visible attention.

What Your Kids Are Actually Learning

Your kids do not understand consumer debt. They do not need to. What they understand is the family's emotional climate around money. And that climate teaches them what's normal long before any school does.

Children of parents in chronic debt typically learn three lessons that follow them into adulthood:

Lesson 1: Money Is a Source of Anxiety

If every conversation about money in your home carries a tight tone, your kids learn that money is dangerous territory. As adults, they may avoid budgeting, avoid checking bank accounts, avoid talking to a partner about finances — exactly the avoidance behaviors that produce more debt.

Lesson 2: Credit Is a Solution

If they grow up watching parents resolve a tight month by adding to a card balance, they learn that credit is the answer to "we don't have enough." Many of them will reach for cards instinctively in their 20s the same way their parents did. The cycle continues.

Lesson 3: This Is Just How Adult Life Works

Maybe the hardest one. Kids who watch their parents quietly carrying debt for years can come to believe that financial strain is the universal adult condition. They don't try for a different reality because they don't know one is available.

Breaking out of consumer debt isn't only about your own peace of mind. It's about what your kids assume is normal when they leave home.

The biggest financial education you give your kids isn't a lecture. It's the tone in your house when bills come in. Whatever that tone is right now is what they're going to recreate in their own house in 20 years.

The Opportunity Cost: What Doesn't Happen

The money flowing to interest is money that isn't flowing somewhere else. Most families know this in the abstract. The concrete version is harder to look at.

For a family carrying $30,000 in credit card debt at 22% APR, the interest charges alone run roughly $550-600 per month. That's $7,000 a year going to interest. Not principal. Just interest.

What does $7,000 a year mean over 10 years of carrying that debt?

- The vacations: Two annual family trips not taken. Ten years of beach weeks, mountain weekends, road trips, summer flights to see grandparents.

- The college fund: $70,000 contributed to a 529 plan over 10 years, growing in market returns, would now be a meaningful dent in tuition. Without that contribution, your kid takes loans.

- The retirement: $7,000/year invested at average market returns for 10 years compounds to roughly $100,000 by year 20. Or doesn't.

- The career move: The night class, the certification, the equipment for the side business — none of that fits the budget when interest is eating $600/month.

- The medical care: The dental work that keeps getting deferred. The mammogram that gets pushed. The kids' eye exams that got skipped this year.

This is the real cost. Not the interest charge on the statement. The life that didn't happen because the interest charge took the money first.

The Health Cost

Financial stress affects physical health in measurable ways. The research is consistent on this.

- Adults under chronic financial stress have higher rates of insomnia, headaches, digestive issues, and high blood pressure

- Major financial stress is correlated with increased anxiety and depression — not as a moral weakness, as a documented physiological response to long-term cortisol elevation

- Marital stress (which financial stress aggravates) is itself associated with worse cardiovascular outcomes and slower recovery from illness

- Families under financial pressure delay preventive medical care, which leads to bigger health bills later

The American Psychological Association's Stress in America survey consistently finds that 72% of Americans report money stress, and roughly a third say money is a major source of conflict in their relationship.

Your debt is not just a financial fact. It's a health risk for the family carrying it.

The Honest Math on Time

Most families with serious credit card debt are paying minimum payments. Here's what that means for the timeline.

$30,000 of credit card debt at 22% APR, paying only the post-CARD-Act minimum (1% of balance plus interest), takes roughly 34 years to pay off. Total paid over those 34 years: approximately $84,000. Of that, $54,000 is interest.

That's three decades of the family's life with this in the background. Three decades of the toll above. Three decades of the opportunity cost.

Compared to debt forgiveness:

- $30,000 enrolled, settled at average 50% of face value across accounts

- Specialist fees at ~20% of original balance

- Total paid over 30-36 months: approximately $20,000-22,000

- Time to debt-free: under 3 years

- Total saved compared to minimum-payment treadmill: approximately $90,000+

For families that fit the forgiveness profile, the difference is measured in hundreds of thousands of dollars and decades of life.

What Actually Lifts the Weight

The toll above doesn't lift gradually as you make minimum payments. It lifts when the debt is actually resolved. When the accounts close. When the statements stop coming.

Most families who finish a debt resolution path report that the change in the household climate was bigger than they expected. The arguments that ended marriages didn't have to end them. The kid who was anxious had a parent who was less anxious. The vacation got booked.

This is the part nobody markets — because it's not really about money anymore at that point. It's about everything money was quietly costing.

What To Do Next

- Take an honest accounting. Write down what you currently spend on debt service per month. Multiply by 12 to get your annual cost. Multiply by however many years you've been carrying serious debt to get the lifetime cost so far.

- Add the invisible cost. What hasn't happened in your family's life because of the visible cost above? Be specific. Vacation. College fund. Retirement contribution. Career investment. Medical care.

- Read the 5 Ways Out. The hub article walks through every path with the honest tradeoffs. Read it here.

- Take the Free Debt Relief Assessment. A senior specialist will compare paths against your actual numbers and tell you what would fit. No cost. No obligation.

Common Questions

How do I bring up the debt with my spouse if we haven't really talked about it?

Start with the cost above, not the blame. Family financial therapists and marriage counselors typically recommend framing the conversation around the future you both want — the vacation, the retirement, the kids' education — and identifying the debt as the obstacle to that future, rather than positioning it as one person's mistake.

What if I'm a single parent carrying this alone?

The toll above is heavier for single-income households because there's no second person to share the cognitive load. Resolution paths still apply — debt forgiveness in particular is often the right tool for single-income families with $10,000+ in unsecured debt. The Free Debt Relief Assessment is the same conversation either way.

Is it actually worth taking the credit hit to resolve the debt?

For most families with serious debt, yes. The "good credit" you preserve by paying minimums forever is good credit you can't really use — you're already maxed on the cards. A 12-24 month credit dip during a forgiveness program followed by recovery beats a 30-year minimum-payment treadmill that drains the family the entire time.

Sources & References

debt.com 2025 Debt and Divorce Survey (42% credit card debt as factor in ending marriage). CNBC Select / National Debt Relief Survey (54% partner debt as reason to consider divorce). American Psychological Association, Stress in America survey (financial stress findings). Federal Reserve consumer credit data. National Endowment for Financial Education research on financial stress and family relationships.

This article is for consumer education only. It is not legal, financial, or medical advice. Your Debt Advocate is not a law firm, financial advisor, or medical provider. A senior debt specialist can review your specific situation through the Free Debt Relief Assessment.

Find Out What Resolution Could Actually Look Like For Your Family

The cost above is real. The path out of it is also real. A senior specialist will run your numbers and tell you what kind of resolution would actually fit. No cost. No obligation. No high-pressure pitch.

Free Assessment

Find out what debt resolution could actually look like for your family.

The interest charge is the visible cost. The vacation that didn't happen, the conversation you didn't have, the lesson your kids absorbed — that's the real bill.