The Debt-Buying Industry, Explained: Why Knowing How It Works Helps You Settle for Less

By Your Debt Advocate · Updated 2026

Most consumers don't know the U.S. debt-buying industry exists, even when they're talking to it on the phone. Knowing how it works changes the conversation — because every step in the process leaves margin that the consumer can recover at the negotiation table.

This is the plain-English guide. How a debt actually gets bundled, sold, and collected. Who the major players are. What the regulators have done. And why understanding the math on every step helps any consumer being chased by a debt buyer settle for far less than face value.

The Six-Step Lifecycle of a Sold Debt

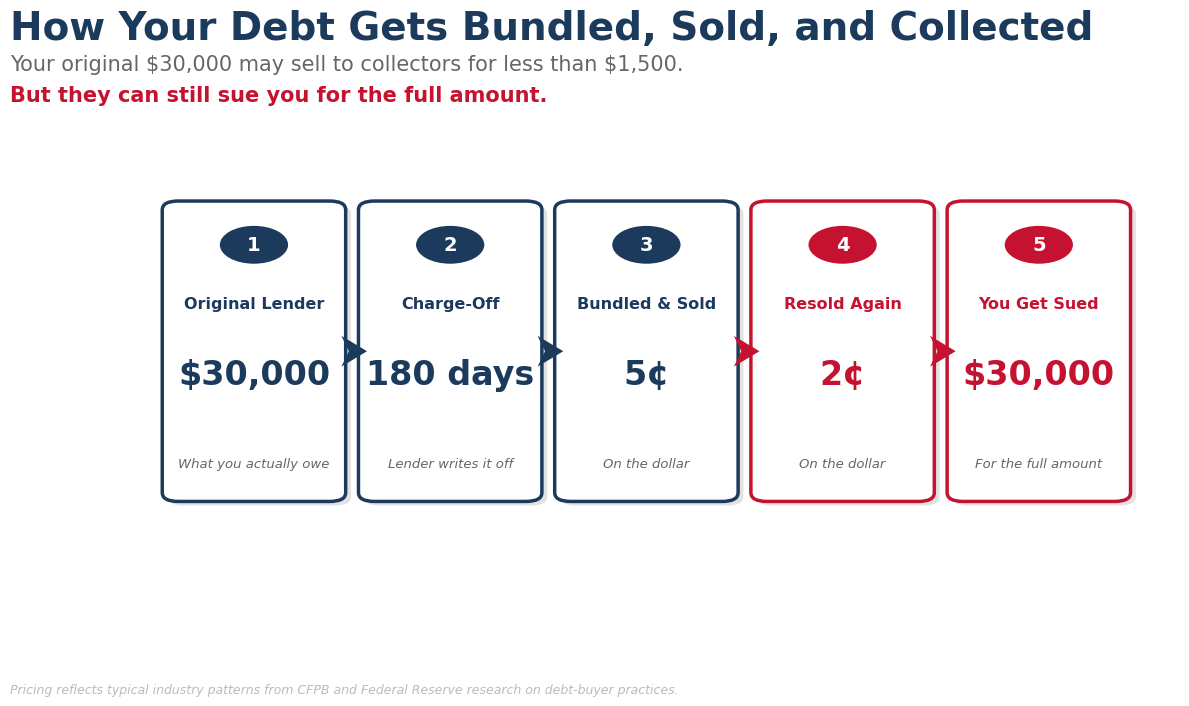

Step 1: Origination & Use $0 paid

You open a credit card account. The card company is the original creditor. You use it. Some balance accumulates. The card company is now extending you ongoing credit, charging interest at the agreed APR, and collecting any minimum payments you make.

Step 2: Delinquency (1-180 Days Late)

You miss a payment. The card company starts internal collection. Late fees apply. Interest rates may increase per the cardholder agreement's penalty APR. The card company expects most accounts to catch up. The Fair Credit Reporting Act sets the seven-year reporting clock from the date of first delinquency.

Step 3: Charge-Off (Day 180) ~5-7% recovery expected

At roughly 180 days delinquent, the card company "charges off" the account — declares it a loss for accounting and tax purposes. The debt is not forgiven; the obligation still exists. The card company simply writes it off as uncollectable from their bookkeeping perspective. Charge-off does not stop collection — it changes who's collecting and how.

Step 4: Sale to a Debt Buyer ~4¢ on the dollar

The card company packages thousands of charged-off accounts together and auctions them in portfolio sales to debt buyers. Per the Federal Trade Commission's 2013 industry study (the most comprehensive public dataset), the average price paid by the nine largest debt buyers was 4.0 cents per dollar of face value across more than 3,400 portfolios studied.

The buyer now owns the right to collect the debt. The card company no longer has any interest in your account.

Step 5: Collection by the First Buyer

The first buyer (one of the major players: Encore Capital/Midland, Portfolio Recovery, LVNV, Cavalry, or others) attempts collection. Letters, calls, sometimes lawsuits. Their collection economics depend on recovering more than the 4 cents they paid — they're targeting recovery of 15-25 cents on the dollar across the portfolio over several years.

Step 6: Resale (Sometimes Multiple Times) ~1-2¢ each subsequent sale

Accounts the first buyer doesn't recover may be re-sold to smaller buyers further down the chain. Each sale further decreases the per-account price. Some accounts trade hands three or four times before they're written off entirely.

By the third sale, the buyer may be paying under a penny on the dollar. Their collection effort is even more aggressive because they have so little invested.

The Math at Each Step (And Why It Matters For You)

Consider what happens to a $5,000 charge-off as it moves through the chain.

- Original card balance: $5,000

- Card company sells to first buyer: ~$200 received (4¢/dollar)

- First buyer attempts collection. They want to recover $750-1,250 across the portfolio's average. They may settle individual accounts anywhere from $1,000 to $4,500 to hit that average.

- If first buyer can't collect, they sell to second buyer: ~$50-75 received

- Second buyer attempts collection. Anything they recover above $50-75 is profit. They may settle for $300, $500, $1,000.

- Third buyer (if applicable): Bought for ~$25. Will accept very low settlements. Aggressive collection tactics.

At every step, the buyer's collection target is some multiple of what they paid — not a percentage of what you originally owed. This is why the same $5,000 face-value debt might settle for $2,500 with the first buyer or $500 with a third-tier buyer. The buyer's math, not your debt's age, drives the negotiation room.

Who's Actually Buying Debt

The U.S. debt-buying industry concentrates around a handful of large players. The most-named in court filings, regulator actions, and credit reports:

Tier 1: The Two Largest

- Encore Capital Group (publicly traded; main brands Midland Funding, Midland Credit Management, Asset Acceptance) — the largest debt buyer in the country

- Portfolio Recovery Associates / PRA Group (publicly traded) — the second-largest

Both have been subjects of formal CFPB enforcement action, twice each. Read the full CFPB action breakdown.

Tier 2: Major Buyers and Holding Companies

- LVNV Funding LLC / Sherman Originator / Resurgent Capital Services — the Sherman group is one of the largest privately-held debt buyers

- Cavalry SPV I, LLC / Cavalry Portfolio Services — major in court filings

- Unifin, Inc. — debt collection agency frequently working contract collections

- Plaza Services LLC and other mid-tier buyers

Tier 3: Smaller Buyers and Resellers

Hundreds of smaller debt-buying firms purchase smaller portfolios, often re-sold from the major buyers. Many operate regionally. Some specialize in specific debt types (medical, telecom, utility). The smaller buyers tend to have less documentation and more aggressive collection methods.

When a collector calls, ask which buyer currently owns the debt and which buyer they bought it from. The further down the chain you are, the cheaper the buyer paid and the more room there is to settle low.

What Documentation Travels With Sold Debt

Here is one of the most useful facts about how the industry works.

When a debt portfolio gets sold, what travels with it is usually a CSV-style data file containing the basic account information — names, addresses, last known balances, charge-off dates, original creditor identity, sometimes Social Security numbers and dates of birth. What does NOT travel with most portfolio sales is:

- The original signed cardholder agreement

- Detailed transaction history showing how the balance built up

- Records of every late fee, interest charge, and dispute

- Copies of every monthly statement

- Records of any prior settlement offers or partial payments

This documentation gap is why the Fair Debt Collection Practices Act validation right is so powerful. When a consumer demands validation in writing within 30 days, the buyer has to produce documentation proving the debt is owed in the amount claimed. Buyers downstream often cannot produce it cleanly.

The CFPB's enforcement actions against the two largest buyers cited specifically that the documentation supporting some collection efforts was insufficient — including affidavits used in lawsuits that were not based on actual document review.

How the Money Flows

For a quick mental map of where the money in the industry flows:

- Original card company: Profits from interest, fees, interchange revenue during the card's active life. Recovers ~4 cents on the dollar at sale to the buyer. Writes off the rest as a tax loss.

- First-tier buyer: Pays ~4 cents to acquire. Targets ~15-25% recovery across the portfolio over several years. Operating margin depends on portfolio quality, vintage, geography, and collection efficiency.

- Second-tier buyer: Pays ~1-2 cents per remaining account. Targets aggressive recovery on whatever they bought.

- Collection agencies on contract: Take a contingency percentage (often 25-50%) of any amount they recover for the buyer.

- Consumer protection attorneys: Earn fees from FDCPA claims when collectors violate the law, often paid by the violating company.

The industry is profitable enough that publicly traded debt buyers generate hundreds of millions in annual revenue. The math works because they're buying loss-account paper at deep discount and recovering even a fraction of face value at scale.

Regulation: How the Industry Is Supposed to Work

Federal law regulates debt collection through several frameworks:

Fair Debt Collection Practices Act (FDCPA)

The foundational federal debt collection law (15 U.S.C. Sections 1692-1692p). Applies to third-party collectors and debt buyers (not original creditors). Limits when collectors can call, what they can say, and what they can do. Provides consumers with the right to demand validation, dispute debts, and send cease-and-desist letters. Statutory damages of up to $1,000 per case for violations, plus attorney fees.

CFPB Regulation F

Effective in late 2021. Modernizes the FDCPA's implementation. Includes call frequency limits (presumptively no more than 7 contact attempts per week to the same consumer about the same debt), required disclosures in initial communications, electronic communication rules, and rules around time-barred debt.

Fair Credit Reporting Act (FCRA)

Governs how debt collection activity is reported to credit bureaus. Sets the seven-year reporting limit on most negative items.

State Debt Collection Laws

Most states have their own debt collection statutes that apply alongside the federal rules. Some are more protective than the FDCPA. Many states require debt collectors to be licensed in the state to collect from residents.

State Statutes of Limitations

Each state sets the time period in which a creditor can sue on a debt. Typically 3-6 years from last activity. Once expired, the debt cannot be sued on (though it can still be reported and called about within FCRA limits).

What Knowing This Changes

Understanding the industry mechanics gives consumers real leverage in three specific ways.

1. Settlement Math Is Real

Knowing the buyer paid pennies on the dollar tells you the floor for what they'll accept is far below face value. Settlements at 30-50% of face value are common. Settlements at 20-30% happen on accounts where the buyer's leverage is weaker (older account, weaker documentation, statute of limitations approaching).

2. Validation Demands Have Teeth

The documentation gap means many buyers cannot validate every account they own. Demanding validation in writing within 30 days of first contact (your right under FDCPA Section 809) sometimes ends the collection effort entirely.

3. FDCPA Compliance Pressure

The CFPB's track record of enforcement against major buyers means buyers face real cost when they violate the rules. Consumers who document violations have leverage. Many consumer protection attorneys handle FDCPA cases on contingency.

The Industry Trends to Know

For consumers and observers tracking the debt-buying industry:

Concentration Among Top Players

The industry has consolidated around the two large publicly traded buyers (Encore and PRA), plus a smaller number of large private buyers. Smaller regional buyers continue to operate but represent a smaller share of total industry purchases.

Increased CFPB Scrutiny

The CFPB has been actively enforcing against the largest buyers, with follow-up actions on consent orders. The trajectory of enforcement has generally been increasing.

Documentation Standards Tightening

State courts have increasingly required better documentation in debt collection lawsuits. CFPB Regulation F clarified requirements at the federal level. The trend is toward more documentation, not less.

Statute of Limitations Variability

Some states have shortened their statutes of limitations on consumer debt over the past decade. Others have not. The patchwork is something consumers in different states should understand for their specific state.

Medical Debt Reform

In April 2023, the three major credit bureaus voluntarily removed paid medical debt, unpaid medical debt under one year old, and medical collections under $500 from credit reports. A broader 2024 CFPB rule that would have removed all medical debt from credit reports was vacated by a federal court in July 2025, so the 2023 voluntary changes are the current state of the rule.

The Bottom Line

The debt-buying industry exists because charge-off accounts are a profitable secondary market for the original card companies. The buyers who acquire those accounts pay pennies on the dollar and target recovery at substantial multiples of what they paid.

That economics gives consumers more leverage than most realize. Validation rights, statute of limitations defenses, settlement math, and FDCPA compliance pressure all rest on the underlying industry mechanics.

For most families being chased by debt buyers, settlement is realistic at far below face value. For many, the documentation gap means the collector cannot prove the debt cleanly enough to win a lawsuit. For some, the statute of limitations has already run out.

Knowing how the industry works is the first step. Acting on what you know — through validation demands, documented communication, settlement negotiation, or FDCPA claims — is the second.

What To Do Next

- Identify which buyer holds your account. Pull credit reports. Check letters and call records.

- Demand validation in writing within 30 days. FDCPA Section 809.

- Check your state's statute of limitations. Old debts may have already aged out.

- Document everything. Calls, letters, contacts. FDCPA violations are worth real money.

- Take the Free Debt Relief Assessment. A senior specialist will apply the industry mechanics to your specific accounts. No cost. No obligation.

Common Questions

How is debt-buying different from collection on contingency?

Debt buyers PURCHASE the debt and own it. They keep all recoveries. Contingency collectors don't own the debt — they collect on behalf of the original creditor or a buyer and take a percentage of what they recover. Many of the calls you receive on charged-off card debt are actually contingency collectors working for the buyer who owns the debt.

Can I check if my debt has been sold?

Yes. Pull free credit reports from AnnualCreditReport.com. The "current creditor" field for delinquent or charged-off accounts will show the current owner of the debt. If it's a buyer name (Midland, PRA, LVNV, Cavalry, etc.), the debt has been sold from the original card company.

Are debt buyers the same as collection agencies?

Sometimes. Encore Capital, for example, owns Midland Funding (which holds the debt) and Midland Credit Management (which collects on it). Some companies do both functions. Others specialize. The legal distinction matters for FDCPA — entities collecting their own debt face different rules than third-party collectors.

If I pay the buyer, does the debt become valid again?

The debt was always valid (assuming it was a real debt originally). Paying doesn't change the validity. Paying does sometimes restart the statute of limitations clock in many states for any remaining balance. Be careful before making any partial payment on an old debt without understanding state rules.

Does the buyer's purchase price matter legally?

Generally no. The buyer is legally entitled to collect the full face value if they can prove the debt and meet documentation requirements. The 4 cents they paid is the buyer's business. It does, however, drive what they'll actually accept in settlement — and that's where it matters in practice.

Is the debt-buying industry going away?

No. It's a profitable secondary market for charged-off receivables. Increased regulation has changed practices but the industry continues to operate. The biggest companies remain publicly traded with strong revenue.

Sources & References

Federal Trade Commission, "The Structure and Practices of the Debt Buying Industry" (2013) — 4.0¢/dollar average price across 3,400+ portfolios. Consumer Financial Protection Bureau enforcement actions against major debt buyers. Fair Debt Collection Practices Act, 15 U.S.C. Sections 1692-1692p. CFPB Regulation F (12 C.F.R. Part 1006). Fair Credit Reporting Act, 15 U.S.C. Sections 1681-1681x. Encore Capital Group (NASDAQ: ECPG) and PRA Group (NASDAQ: PRAA) public financial filings.

This article is for consumer education only. It is not legal advice. Your Debt Advocate is not a law firm. Federal and state laws on debt collection are complex and case-specific. A consumer protection attorney can advise on your specific situation. A senior debt specialist can review your situation through the Free Debt Relief Assessment.

Apply What You Know to Your Specific Situation

Understanding the industry mechanics is the first step. A senior specialist can apply them to your specific accounts and tell you what realistic resolution looks like. No cost. No obligation.

Free Assessment

Apply the industry mechanics to your specific accounts. A senior specialist will tell you what's realistic.

The buyer's math, not your debt's age, drives the negotiation room. Once you know how the math works, you know where the floor really is.